Claiming ETI

The ETI calculated is used to reduce an employer’s PAYE liability for a given month and is reflected on the EMP201 along with any ETI carried forward and the amount of ETI utilised. This article outlines when ETI is carried forward, how long it can be claimed for and how ETI is reported on the EMP201.

ETI Carried Forward (Roll-Over Amounts)¶

Where the PAYE amount is lower than the ETI, the employer’s PAYE liability will be 0; any ETI not utilised is carried forward to the following period.

Where the PAYE exceeds the ETI, the full ETI may be used to reduce the PAYE liability and nothing will be carried forward.

SARS stipulates that ETI may not be carried forward to March or September; therefore, you will notice that ETI Brought Forward will always be R0.00 on the EMP201s for March and September. Any ETI Carried Forward and, therefore, not utilised at the end of February and August each year will need to be claimed back from SARS.

ETI Claim Period¶

ETI may be claimed for 24 months per qualifying employee and these 24 months need not be consecutive or correspond to the employee’s months of employment. Where an employee has separate contract periods with a single employer, the ETI month they are in will follow on from the previous contract period. Similarly, if an employee is transferred between companies that are associated persons*, the months must be counted as if they had not moved at all.

*An associated person is any entity in relation to each other which is directly or indirectly managed or controlled by substantially the same person (e.g. two subsidiaries under a holding company). Where an employee moves between companies (who are part of a group) with the same PAYE reference number, for ETI purposes this will be deemed to be continuous service by the employee and the ETI will continue and not start again.

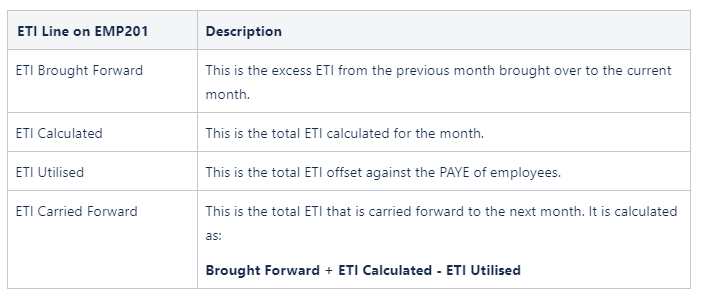

ETI and the EMP201¶

The EMP201 is used to report ETI, along with PAYE, UIF and SDL. The ETI is reported under four categories:

Example¶

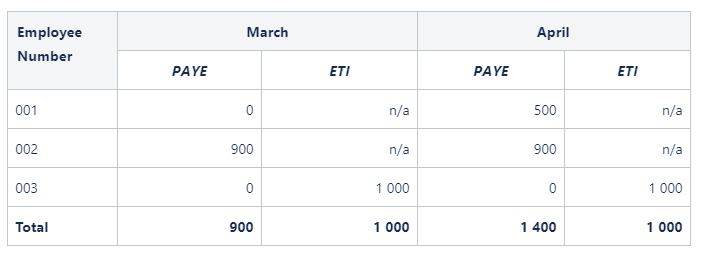

A company has three employees. The employees have PAYE and ETI calculated as follows for March and April:

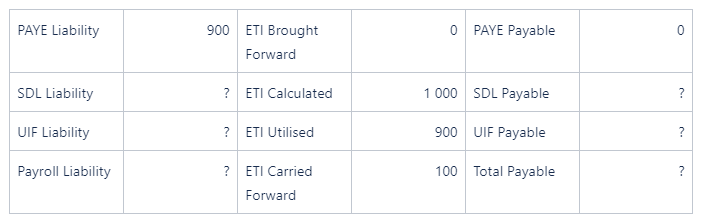

The EMP201 for March will look as follows:

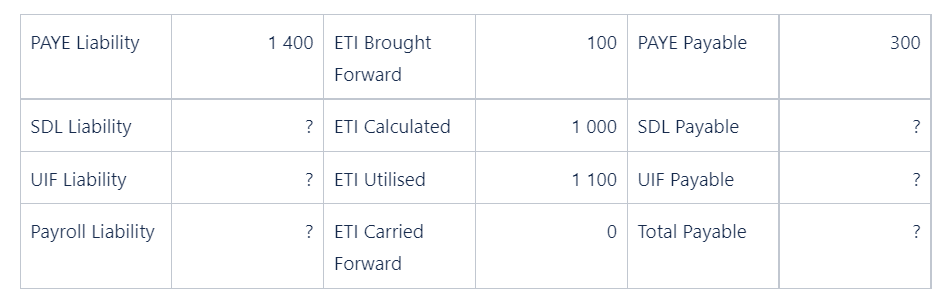

The EMP201 for April will look as follows:

In March, R1 000 of ETI is calculated, but only R900 can be used since the PAYE liability is only R900. The difference of R100 is rolled over to April. In April, the R1 000 ETI calculated plus the R100 rolled over amount from March is used to offset the R1 400 PAYE liability. The PAYE payable to SARS is the difference of R300.