Calculating ETI

This article provides information on how ETI is calculated.

ETI Tables¶

The value of the ETI the employer may claim per qualifying employee depends on the amount of the monthly remuneration paid to each of them. Employees’ remuneration can fall into one of three brackets, each with its own calculation. Furthermore, different calculations apply in the first and second years of the incentive.

| Monthly Remuneration | ETI per month during the first 12 qualifying months | ETI per month during the second 12 qualifying months |

|---|---|---|

| R0 – R2 499.99 | 60% of monthly remuneration | 30% of monthly remuneration |

| R2 500 – R5 499.99 | R1 500 | R750 |

| R5 500 – R7 499.99 | R1 500 – [0.75 × (monthly remuneration – R5 500)] | R750 – [0.375 × (monthly remuneration – R5 500)] |

Counting the qualifying months

In determining the first or second 12-month period, only the months in which an employee was a qualifying employee are taken into account. For example, an employee may be a qualifying employee in their first three months, but not a qualifying employee in the fourth and fifth months. If the employee is a qualifying employee in their sixth month, the sixth month is then seen as month number four as far as the 12-month period is concerned.

Employees Working Less than 160 Hours per Month¶

Where an employee is employed for less than 160 hours in the month, the remuneration amount must be “grossed up” to 160 hours per month to calculate the value of the ETI. The ETI amount claimable can then be determined and “grossed down” in the same ratio. The ratio is determined by dividing 160 by the number of actual hours employed (discussed below).

Example - Employed for less than 160 hours per month

An employee works for 80 hours per month and earns R1 500. The employee is in their first 12 months of employment. The ETI is calculated as follows:

| Steps | Calculations |

|---|---|

| Step 1: Gross up the remuneration | R1 500 × 160 ÷ 80 = R3 000 |

| Step 2: Determine the ETI on the grossed up remuneration | ETI for an employee earning R3 000 in their first qualifying 12 months = R1 500 |

| Step 3: Gross down the ETI | R1 500 × 80 ÷ 160 = R750 |

Remuneration¶

Prior to 1 March 2022, Remuneration for the purposes of calculating ETI followed the same definition of remuneration as defined in the Fourth Schedule of the Income Tax Act. Remuneration in the Fourth Schedule includes all income (including commission and overtime), benefits, and taxable allowances.

As from 1 March 2022, remuneration for the purposes of calculating ETI has been amended and is now determined as follows:

Remuneration (as defined in the Fourth Schedule) less Benefits less Non-BCEA Deductions.

Non-BCEA Deductions are all those that are not considered BCEA Deductions. BCEA Deductions include statutory payroll deductions, such as PAYE and UIF, court-ordered deductions, such as arbitration awards or maintenance orders, and other legislated deductions, such as medical aid, retirement funds, and any fees prescribed by a bargaining council (e.g. union fees, sick fund fees).

Classification of Built-In System Items¶

The following list outlines the classification of built-in system items that are considered deductions:

| BCEA Deductions | Non-BCEA Deductions |

|---|---|

| Garnishee | Repayment of Advance |

| Income Protection | Loan Repayment |

| Maintenance Order | Staff Purchases |

| Medical Aid | |

| Pension Fund | |

| Provident Fund | |

| Retirement Annuity Fund | |

| Union Membership Fee | |

| Voluntary Tax Over-Deduction | |

| Donations |

Please note that although every effort has been made by SimplePay and other industry bodies to ensure that this list is correct in all respects, SARS has stated that they cannot currently confirm the classification of deduction items. The classification could, therefore, change at a later date.

Classification of Custom Items¶

If you have any custom deduction items that are a copy of an existing built-in system item, these will be classified in the same way as the system item that it is based on.

All other custom deduction items will be considered non-BCEA deductions by default. If you wish to change this, this will need to be configured. Please see step 2 in the following help article for more information:

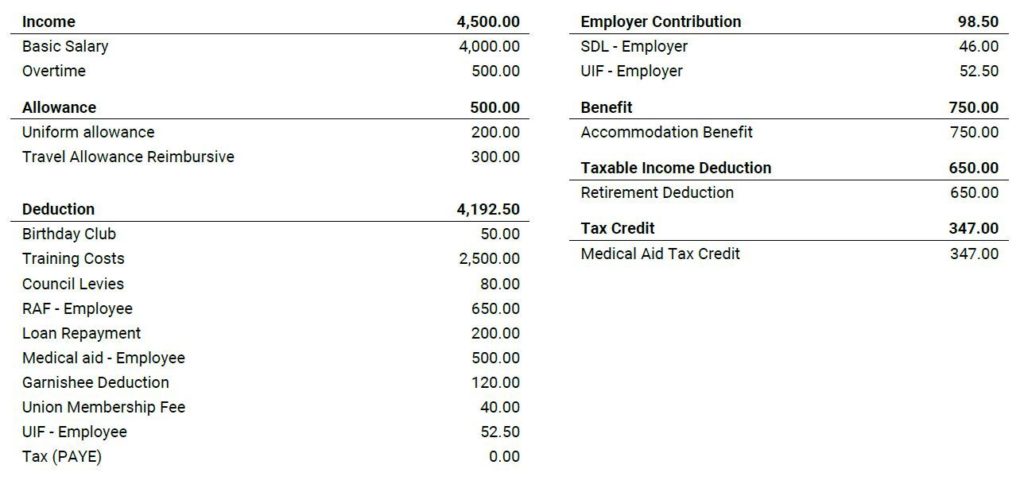

Example - Remuneration for ETI

An employee has the following items on their payslip:

ETI Remuneration would be calculated as follows:

Step 1: Calculate remuneration

= Income + Benefits + Taxable Allowances

= R4 500 + R750 + R0*

= R5 250**

*Both allowances are non-taxable allowances

**This is the ETI remuneration as calculated prior to 1 March 2022, prior to the amendments

Step 2: Calculate ETI remuneration

= Remuneration – Benefits – Non-BCEA Deductions

= R5 250 – R750 – R50 (Birthday Club) – R2 500 (Training Costs) – R200 (Loan Repayment)

= R1 750

Actual Hours Employed¶

When determining whether an employee is employed for at least 160 hours during the month, the following calculations are done:

| Fixed Salaried Employees |

|---|

| Actual hours employed = Scheduled hours as per Regular Hours screen + Additional normal hours – Unpaid leave – Short hours |

| Hourly Paid Employees |

| Actual hours employed = Normal hours captured for Basic Salary under Payslip Inputs (the Regular Hours screen is ignored) + Sunday hours + Public holidays worked + Public holidays not worked but paid for + Hours of paid leave |

Note

While overtime is included in the remuneration calculation, the hours are not included in the actual hours employed. As per the Binding General Ruling (ETI) 44 (Issue 2), the 160 hours stipulated in section 4(1)(b) must consist of only ordinary hours of work and do not include overtime or hours other than ordinary hours of work.